![Single Mums Business Network [SMBN CIC]](https://singlemumsbusinessnetwork.com/wp-content/uploads/2022/07/cropped-asset-sq-1.png)

You can download the pdf of the Social Impact Review Report above, but I have copied the content below for ease of reference.

Single Mums Business Network

Social Impact Review

- Barriers to Work, Cost to Economy and Solution

- Barriers to Finance, Cost to Economy and Solution

- Barriers to Home, Cost to Economy and Solution

- Stigma, Misconceptions, and Ignorance

Barriers to Work, Cost to Economy and Solution

Most women, following reproduction, face barriers to work that did not exist prior to becoming a primary carer.

Barriers

Drawing on my own personal experience I had a strong work ethic from age 14 when I began working part-time, I worked full-time immediately following my GCSE’s for 20 years prior to starting a family age 35. I had full expectation of maintaining a full-time salary albeit with a little flexibility, and being self-sufficient whilst continuing to pay my mortgage which at this point was 10 years and £60K down the line.

During maternity leave, when my request for flexible, or pro-rata, slightly reduced hours was declined, due to the full-time hours being required to suit the needs of the business under my job description, along with not wanting to set a precedent for other members of staff who may want to work flexibly, I found myself in a situation where I had to advise I would not be returning to work, simply due to the logistical problem of fitting work and the commute into childcare hours. Whilst some women will have (physical) co-parenting or grandparent support, millions do not, including those in marriage.

I was not too concerned initially as I had several qualifications and a strong work ethic and so I confidently went about searching for work that would support my needs as a primary carer to work a little more flexibly. This was when I was faced with the reality of suddenly entering a job market with millions of other, intelligent, capable, experienced, and qualified mothers, all needing this flexible / pro-rata work. I found work but it was incredibly low pay, under market value for the level of responsibility, due to the high demand for part-time work. Consequently, I needed to apply for Income Support, Housing Benefit, Council Tax Reduction, and I was living in relative poverty without a reasonable food budget, let alone any disposable income. In a short space of time my home was repossessed, and I was trapped in the private rental sector, further increasing my outgoings and need for benefits.

As I continued to search for work in line with my skillset and salary scale I was met on a daily basis with hundreds of social media posts inviting me to work for free, for companies with zero corporate responsibility with respect to the supply chain or Modern Slavery Act, under the ruse of self-employment, or I was invited to work in the care sector, which, whilst is an incredible thing to do, is low paid and often underutilises your skillset.

Cost to Economy

The cost to the economy is evident. Instead of paying tax on a full time or 0.7FTE wage, I was in receipt of benefits, the long-term impact of this will be more evident throughout this review.

Solution

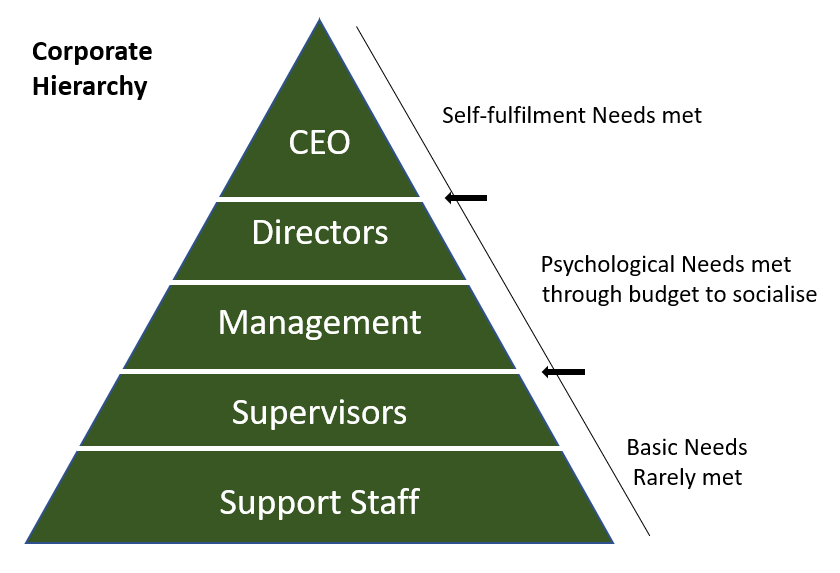

When I worked in Tenerife in 1998 the local government enforced a law that meant any ex-pat business had to employ a 20% local workforce, to ensure their native Canarians were not at a professional or financial disadvantage. It would be reasonable to ask the UK Government to introduce similar legislation to ensure that we do not suffer a disadvantage because of being a primary carer. It is presenteeism that drives benefits and costs the economy billions. Legislation would need to ensure at least 30% of the UK workforce are employed 0.7 or 0.8 FTE in every pay scale. Where flexible and part-time working does exist currently, it is mostly an option for support staff and not senior employees. Support staff are more likely to be on a lower wage and consequently are more likely to need universal credit to top up their income.

The real drivers of universal credit are the companies who have a pay scale that does not support levelling up the Country and UK economy, and insist on 9-5, 8:30 – 4:30, 9-5:30 or later with an hour for lunch. If you cannot commit to these hours you are often locked out of work in line with your skillset and salary scale that you have previously worked towards achieving.

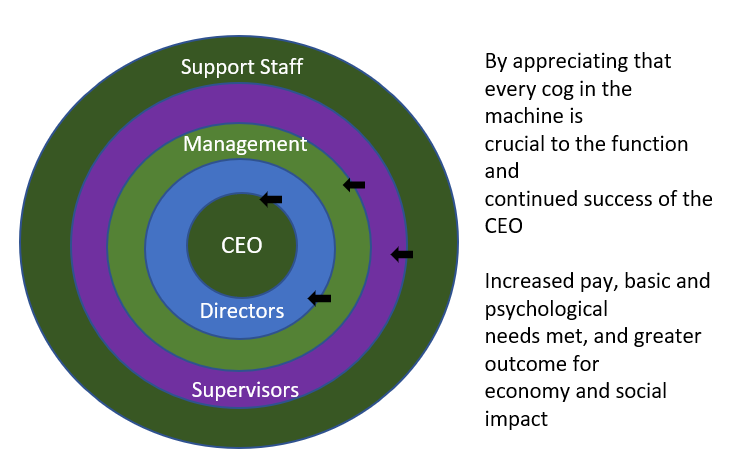

We need to reformulate the company pay structure to visually support the circular economy, rather than the hierarchy economy. These companies would then have corporate responsibility for social impact and the UK benefits bill would be reduced by billions.

Equally we need to explore the possibility of a more modern school year. We no longer need children to work the farms on the summer or stay home in the heat. We are in the 21st Century, but still operating as if it were the 19th Century.

It is extremely easy to see how a circular corporate structure would support a circular economy. The thinkers would not have an operation without the doers. We need to level up salaries and remove any structure that leaves the entry level or support staff without sufficient basic needs. This is relevant for every UK employee currently living in relative poverty because of a pay scale that is not in sync with the cost of living. Capitalism = benefits = cost to economy.

Barriers to Finance, Cost to Economy and Solution

Barriers

Once you enter a world of low income, relative poverty, and without means to put by disposable income for a rainy day, your barriers to finance increase significantly. Consequently, your level of debt further increases when life has a habit of facing you with unaffordable essential expenditure, and you end up in a trap that leaves you, and the economy, in tatters. Again, drawing on my own personal experience. Once I faced the barriers to continue my self-sufficient salary, in quick succession my home was repossessed, my credit file damaged to such a degree that I could not access affordable consolidation or rainy-day loans, and my only options were high interest loans, pay day loans, and other high interest borrowing. These loans were not used for luxury living, short breaks or big screen TV’s, they were used to cover essential bills, rent shortfall, and food. I was advised to declare myself bankrupt on several occasions, but my adversity did not sway my pride, and desire to repay all borrowing in full. I did not want to have a negative impact on the economy or supply chain, and with help entered arrangements to pay debts long-term rather than write them off. But I understand why people do write them off, as often it is unethical, capitalist lending that leaves you vulnerable to loss of life if you do not evidence the results of high interest lending.

Consequently, with a determination not to be reliant long-term on benefits as a result of low pay and high rent, I persevered with setting up my own company and working on a self-employed basis, alongside part-time work, studying a law degree and solo parenting. But of course, the credit score and lack of asset security, meant that banks and other high street lenders would not help me escape the financial pit of relative poverty and I was judged only on credit score, not on work ethic, acumen, or business potential. These barriers to finance resulted in me being unable to kickstart my business and walk away from needing to claim income support.

Cost to Economy

Again, it is clear how financial barriers cost the economy. From the costs of bankruptcy to the long-term need for benefits due to financial adversity. Already pensions are affected.

Solution

There are many ways to resolve the financial barriers that exist. Regulation of loans and cost of living alongside access to business finance and greater business support. Many women choose self-employment as a measure to continue working when society makes it very difficult for you to earn a living in line with your skillset in the sanctuary of employment security, pensions, and corporate responsibility. If the work force unwittingly holds primary carers back due to presenteeism and capitalism the UK must do better to help people help themselves generate a reasonable salary when they have a strong work ethic. The first solution would be to address the credit scoring system that leaves millions of people without access to finance. The UK is particularly good at offering student loans and it would serve well to offer similar self-employment or small business loans. As with the bounce back loans, the bank could be obliged to lend to those in financial hardship with the promise of government underwriting. The best possible thing the Government can do is remove financial barriers and stop banks from holding people back from helping themselves. This money can either be recovered from company income, wages, or worst-case scenario benefits, as some other small loans are. But C19 has helped millions of UK constituents see that universal credit would never be a lifestyle choice by anybody who has ever drawn a wage, and that it is a truly degrading, humiliating and unsustainable way of living, if you want any life at all. This would save the economy billions in the long-term on benefits, and until the last breath, pension credits.

Equally more attention needs to be given to bank charges, and higher cost of bills due to lower income. To elaborate, when you earn a higher wage and have disposable income you are likely to pay your bills annually, or quarterly, from Council Tax, Car Tax, Home Insurance, Car Insurance, TV Licence, Water and Electricity. When you have been unable to budget for these due to living without disposable income, you have to pay these monthly, when you pay these monthly, you pay more for the ‘privilege’ of doing so. When you are paying bills monthly in adversity, normally this has to be by Direct Debit. If you pay by standing order you can easily move the payment by a couple of days if you are without means, which is often a reality when you live with negative income, in work poverty. Consequently, unable to self-manage direct debits, banks will charge you for unpaid direct debits, the company will also charge you for unpaid direct debits, because it is more administration for them, instead of you. With the reality of so many in financial hardship, we need to understand that this is not poor money management, this is poor governance of income v cost of living, and inability to have the autonomy to manage one’s outgoings on a weekly basis without incurring charges.

Banks profit from poverty and refuse to help people out of poverty. This all costs the circular economy and has negative social impact. Disposable income is spent in the economy. Charges and debt cost the economy by increasing the need for benefits and debt relief.

Barriers to Home, Cost to Economy and Solution

Barriers

Entering a world of low pay or barriers to finance leaves you in a situation where you consequently face barriers to home. Again, drawing on my personal experience. I had worked for a decade prior to securing my first mortgage and I paid my mortgage for a decade prior to having to enter a world of low paid work and needing a benefit top up in order to survive. Due to the simultaneous adverse credit score I faced significant barriers to home. As part of my career journey I was a qualified estate and letting agent, and I not only witnessed, but was instrumental in, discriminating against prospective tenants with poor credit score or in receipt of benefits, and pricing both sale and rental property, at a rate that was pleasing only to the landlord or vendor, without real Governance or understanding in my twenties of how this would adversely affect the economy long-term, leave very vulnerable people destitute, and support the long-term rental trap. I am pleased that I was duly punished for this with my own experience. I returned to the same estate agent that I worked for when I was a married homeowner, and landlord, a year later as a single mum on benefits, with a poor credit score and without a guarantor, begging for an affordable property for myself and my daughter, after already being turned away by every other estate agent, and knowing fully why. They did not help me. I had to turn to private, accidental landlords, who advertised in press rather than through an agent. Consequently, these landlords / homes, were either more expensive, short-term, in poor condition, or unethical or unsafe in some other way. I moved several times with my daughter, always paying my rent, albeit with the help of pay day loans, with the constant lack of understanding from those closest to me. Asking why I lived in an expensive house instead of an affordable town house or why I was moving again, they did not understand that the affordable, long-term, secure town houses were let to those who looked good on paper, and without a guarantor I was turned away, over 100 times during 6 years of begging.

Of course, my frustration, was that if I had had some help with my mortgage, I could have saved my home, my own estate, my child’s secure future, if there was help in this way I did not know about it. The UK creates booklets of advice for some minority groups, and I think if a similar booklet had been given to me in the maternity ward, the cost to the economy would have been significantly reduced.

Cost to the economy

Because of this rental trap, I needed benefits, the cost to the economy is clear, but when I was eventually awarded a social housing tenancy, my income covered my rent, and so I no longer needed housing benefit, so was it me on benefits, or my landlords. Landlords who profited and gained estates at the cost of the taxpayer. My rent was £200 more than my mortgage, every month for six years.

The cost to the economy over a lifetime is significant. It is not only the cost of needing to apply for housing benefit to pay private rent, but also the long-term impact of that private rent leaving the tenant without disposable income, without means to improve the credit score, without means to apply for or save for a mortgage, yet the monthly outgoings of private rent are often equal to, or more than, monthly outgoings for a mortgage. This means reduced means to save a pension, and this means paying rent to the last breath.

Solution

If you remove barriers to homeownership, you remove the need for housing benefit and pension credits in later life. Of course, nobody would want benefits to buy somebody a house, although it is arguable that benefits are exactly what buy landlords houses. It is reasonable to set a standard for a person to evidence a decade of work, tax contributions, and ability to pay rent before they become a homeowner, at least then if they do fall on hard times and need benefits, they are still paying into their own estate and not that of another person. The long-term saving to the economy is great, and after a decade of payslips and financial autonomy nobody will choose benefits long-term. If a person can pay their own mortgage for 20 or 30 years, they can then spend disposable income into the economy for the last 1/3 or 1/4 of their life. If they do not have a mortgage, they will be struggling to pay rent in their 60’s, 70’s, 80’s 90’s and so on. This will have an impact on each generation in that family, without inheritance, security, or the bank of mum and/or dad to help them.

Equally, governance of the private rental sector. This has come a long way with respect to discrimination and fees (albeit discrimination remains subtle), but price setting is ungoverned. Private rent is a capitalist enterprise, which could at the very least offer grounds for a mortgage where deposit or credit scoring is adversely affected due to barriers to finance and work in sync with salary and skillet. The Government have offered to grants to landlords, but this money could be used to put the estate in the rightful hands of the one paying for it. Credit scoring and barriers to deposit have a lifetime affect on the economy and carries a greater penalty than bankruptcy or manslaughter.

We must accept that houses are no longer £7000. We no longer live in a society where a man’s wage will pay for the cost of living, whilst his wife takes care of all childcare, school holidays, cleaning, cooking, sick days and so on and has equal share to his pension and permanent stability as a result. We live in a society where 1 in 4 households with dependents are single households. One salary no longer enables the cost of living or provides the opportunity to save a mortgage deposit. And women are no longer able to cover school holidays on top of full-time work, pension, homeownership, and high private rents. We need to make it okay for one salary to cover one cost of living, otherwise we force people to remain in abusive relationships and make adults less accountable for their behaviour and marriages hard to leave. A marriage should be a happy place, and a financial benefit, not a financial necessity.

Stigma, Misconceptions, and Ignorance

Stigma

It is often perceived that a single mum has made bad choices, that she has made a lifestyle choice, and that she is a single mum because she is work shy or uneducated. We must challenge this and help to raise awareness that most of us have a strong work ethic, happy and healthy children, and are single by being divorced or widowed after trying to do it by the book.

Misconceptions

We do not need upskilling, we need barriers removed so that we can use our skills, we do not need a rich man, we need barriers removed so that we can create our own stability and estate, we do not need apprenticeships, we need work in sync with childcare. We do not need charity; we need access to 100% finance to build our own business regardless of adversity.

Ignorance

When I refer to ignorance, I never mean to cause any real offence, ignorance is simply lack of knowledge or experience. I was ignorant and was still a perpetrator to these barriers in my early 30’s. If you do not understand what holds people back and how easily that can be changed that is forgivable, but once you know, you must do something about it. These barriers are created by society. These barriers can be removed by governance of society.

Closing word

Thank you for reading the Social Impact Review created by the Single Mums Business Network, UK. Crucially many of us are in business as a measure to make work work as a primary carer. We do not want to suffer financial hardship because of procreation, and we are doing all that we can to be financially self sufficient whilst working hard to ensure that these barriers do not equate to long term cost to the economy. Until things change there are many ways that the Government can help us to succeed in self-employment and we would welcome an audience to discuss that. We can contribute to the UK economy; we can be considered for public sector contracts and we can import and export where we are in manufacturing or supply goods or services. We also need protecting from ungoverned unethical recruiters who enjoy great profit without corporate or social responsibility. We are fighting to build our own pension and provide some stability for our children. Whilst this document is relevant to all primary cares, single dads, and parents in marriage, the focus here is on the 90% of single parents and primary carers in the UK who are women, but it hopes to have a positive impact in reducing barriers to all, regardless of sex or status.

(c) Copyright Single Mums Business Network 26th February 2021